How to Organize Your Personal Budget?

Discover how to organize your personal budget using realistic methods. Learn how to handle supermarket expenses, exercise self-control, and build your investment capacity.

Cezar Pimentel

2/26/20263 min read

The foundation of wealth building starts with structuring an efficient individual cash flow. Organizing a personal budget isn't a mere recording of expenses, but the application of a resource allocation methodology that allows for predictability, control, and the generation of surplus for investments.

Cash Flow Mapping and Inflation Control

The first methodological step in financial planning is an exact diagnosis of income and expenses. This requires classifying living costs into fixed and variable, as well as understanding the continuous impact of official inflation (CPI) on monthly purchasing power. The central goal of this stage is to establish a positive savings margin, often using strict rules for the percentage distribution of income.

The Supermarket and Everyday Microeconomics

Within this mapping, the supermarket has consolidated itself as one of the biggest villains in the average person's budget. Macroeconomic factors directly affect the cost of basic groceries, a reflection we frequently address in Market News: The impact of interest rates, inflation, and the economic scenario on the investor's pocket.

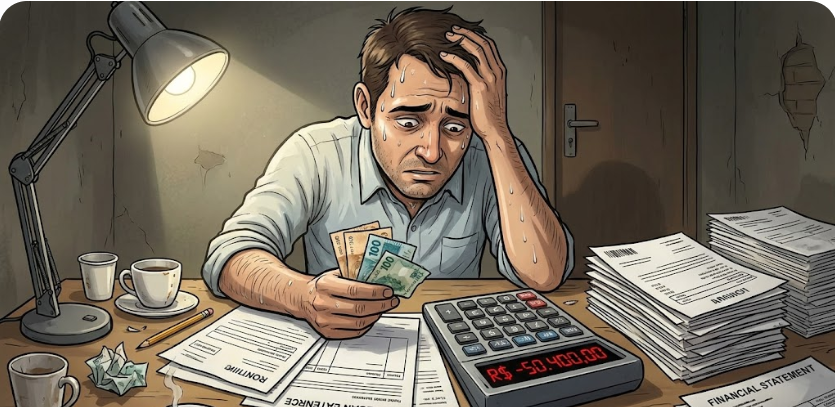

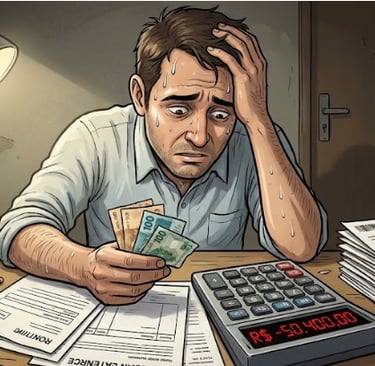

Faced with the rising cost of food, the first behavioral reaction is usually resistance: "I won't give up something I like to save pennies." However, financial math is ruthless with pennies. When accumulated against you at the end of the month, they make a brutal difference.

Giving up a small luxury today for a conscious choice—and not out of pure necessity or lack of money—is the ultimate demonstration of financial self-control. It's you saying right to the face of your own consumption impulses: "I'm the boss here!". To optimize this expense line, three pragmatic measures are necessary:

Pragmatism on the Menu: Have the "stomach" and resilience to consume repeated meals. Batch cooking drastically reduces financial waste and optimizes your routine.

The Reality of Time and Budget: For those with a tight budget and a rushed daily life, the demand for a 100% fresh menu often doesn't fit reality. Ultra-processed products only cause extreme damage when consumed in absolute excess. Financial efficiency often requires choices based on the reality of time and cost, preventing the pursuit of an idealized diet from destroying your cash flow.

Material Detachment and the "Dream of Homeownership": Only own valuable items that you can afford to lose or replace without missing them or going broke. The market frequently romanticizes the "dream of homeownership", but housing is, at its core, a basic need. Categorizing it as the sole ultimate goal to be achieved for well-being can lead to the immobilization of all your capital, stifling your financial future.

Liability Restructuring and Deficit Elimination

If the initial diagnosis reveals a negative balance, the absolute priority becomes stopping the capital bleed. Debt renegotiation and surgical expense cutting are essential. To understand the complete mechanics of interest reduction and payment prioritization, check out our Savings Tips: How to organize your budget and get out of debt.

Building Liquidity and Emergency Funds

Once the deficit is neutralized and consumption is controlled, the allocation of the surplus must be directed towards risk mitigation. Building an emergency fund protects the individual from having to resort to expensive credit lines. To allocate this capital, it is necessary to look for vehicles with high liquidity. We detail the ideal tools for this purpose in our guide on Fixed Income: Government bonds, CDs, and security strategies.

Capital Flow Directed to Assets

With a stabilized budget and an established emergency fund, financial planning enters the asset accumulation phase. For investors focused on monthly income, Real Estate Investment Trusts (REITs): Dividend analysis and how to invest offers the necessary structural overview. For those seeking diversification and capital gains, reading Stocks: Evaluating specific companies and stock exchange sectors details the dynamics of publicly traded companies.

Organizing your budget requires short-term sacrifices, but it is the essential mechanism that funds your definitive transition from debtor to investor.

(Legal Notice)

Investments involve risk, and past performance is not a guarantee of future results. We do not make direct recommendations.

ConTATO

Cezar Pimentel

Crypto expert

Editor and writer for Money Bridge.

Contribute to our blog:

Wallet Lightning: knownworm12@walletofsatoshi.com

Chave Pix: 635af7b7-92ab-4b5a-a7d3-541d3fd41701

Bitcoin On-chain: 1D1dbDJiQKuLLcWCH2M2yVjArWj3yCufmn

USDT Polygon: 0xb83948456f41cb8b0f8528472558d7fe977cd4c9

USDT TRC20: TBKMFK9BGudeEsaXwL3z9dnQC8nakFrKAM

USDT BEP20: 0xb83948456f41cb8b0f8528472558d7fe977cd4c9

USDT SOL: 3afEJTg2oDbXf6diL5SUf4g87S13hyWtXcsJxde8XzAn

USDT TON: UQDeeyyGHoXCW18QcNCElonzmntgzeki3rtqqN8zZnNDMtLO

USDT Arbitrum one: 0xb83948456f41cb8b0f8528472558d7fe977cd4c9

Acceptance of Terms – Money Bridge